The government’s revised Help to Buy Equity Loan scheme for home buyers is now open for applications from first time buyers in England. The scheme replaces the current one, and will run until March 2023.

Help to Buy has proved popular since its initial launch in 2013, with nearly 300,000 homebuyers purchasing their first property through the scheme. The new scheme will replace the old one from April 2021 but is already open for applications.

Eligible first time homebuyers can buy a property with as little as 5% deposit.

How does it work?

Homebuyers must prove that they have saved enough deposit to cover the 5% deposit. In exchange, the government provides a low interest loan, the value of which varies between regions. The remaining purchase funds come from a mortgage on the property.

Am I eligible?

You can only join the scheme if you can meet all of the following criteria:

- You (and your partner, if you have one) must not have owned or currently own a property or residential land in the UK or overseas.

- The home must be a newly built property, purchased from an approved developer that is registered with the scheme.

- The property must be your only home, as well as your permanent residence.

- You must show that you have saved the minimum 5% deposit and that you can afford to make monthly mortgage payments as well as interest repayments on the Equity Loan.

How much can I borrow?

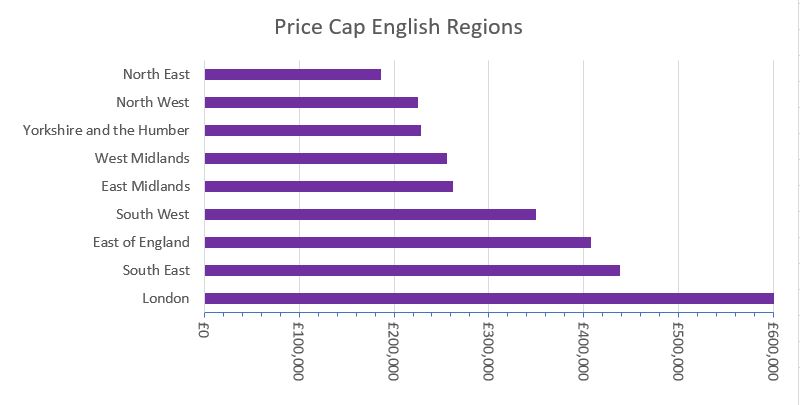

The government provides a low interest loan worth up to 20% of the price of the property (40% for properties located in London). The purchase price is limited and varies between regions. The price caps set up to March 2023 are:

When do I start to pay for the loan?

For the first five years, the equity loan is interest-free and you pay a £1 management fee each month.

Interest-only payments begin in the sixth year but this means the capital is not reduced. However, you can repay all or part of your equity loan at any time as long as the payment is at least 10% of the current market value of the property.

From the sixth year, interest is charged at 1.75% per month, rising each year by the Consumer Price Index plus 2%.

The loan is repayable when you sell your home, when you pay off your repayment mortgage or at the end of the equity loan term.

If you sell the property for a greater or lesser value than you paid for it, you will still repay the same percentage of the sale price as you borrowed – so you may pay back more or less than the amount you borrowed.

More information on the Help to Buy equity loan scheme in England is available from the Help to Buy website.

Help to Buy Wales

The Welsh government has extended its Help to Buy scheme to March 2022 but it may be extended further in the future, possibly to match the English scheme’s March 2023 deadline.

As in England, the Welsh Help to Buy Wales Equity Loan scheme allows home buyers to purchase a property with a 5% deposit and 75% mortgage. The remainder is funded using a 20% equity loan funded by the Welsh government.

Welsh home buyers can join the scheme if they can meet the following criteria:

- Existing home owners and first time buyers are eligible to join the scheme.

- The property must be your only home, as well as your permanent residence.

- Buyers are required to provide a minimum deposit of 5%.

The maximum property value in Wales is £300,000 for new builds and the property must be built by a housebuilder taking part in the scheme. In Wales, the maximum amount of equity loan is £60,000.

As with the scheme in England, a monthly administration fee of £1 is payable from the date you join the scheme. No other charges are made for the first five years, but in the sixth year interest is charged at 1.75% per annum on the loan which will increase every year by the retail price index plus 1%.

The loan is repayable on the sale of the property or after 25 years if you still own the property. If you sell the property for a greater value than you paid for it, you may have to repay more than you borrowed.

Help to Buy Scotland

The Scottish government has extended its Help to Buy scheme to March 2022 but this may be further extended to March 2023, as in England.

Scottish homebuyers must fit certain criteria to be eligible for the scheme in Scotland:

- Existing homeowners may join the scheme alongside first time buyers, but if you own a property already you must sell it before you purchase another property using the Scottish Equity Loan.

- The property must be your only property and you must live in it.

- The property must be built by a housebuilder who is affiliated with the scheme.

In Scotland, the maximum equity loan value is 15% of the property purchase price and the maximum purchase price of the property is £200,000. Homebuyers must pay a minimum 5% deposit and tThe mortgage from a participating lender must be a repayment mortgage, not an interest- only first mortgage.

A financial assessment is made to ensure that your housing costs (i.e, mortgage, charges and fees) are no higher than 45% of your net disposable income. You cannot choose to make lower mortgage payments than your income assessment which will be based on 4.5 times your income if you are buying the house on your own, or 3.5 times your joint income if buying with another person.

The loan is repayable at any time but, if you sell the property for a greater or lesser value than you paid for it, you will still repay the same percentage of the sale price as you borrowed so may pay back more or less than you borrowed. There is no ongoing interest payment due after five years and you can ‘staircase’ purchase a greater share in the property up to a minimum 5% of the market value each year.