In 2006, the percentage of people living in Britain aged 65 or older was 15.9%. That increased by 13% to 18% in 2016, according to the census survey. The Office of National Statistics predicts that, by 2036, over half of local authorities will have a local population aged over 65 in excess of 25% – and there will be a national average of 25% of the population aged over 65 years old by 2046.

In 2006, the percentage of people living in Britain aged 65 or older was 15.9%. That increased by 13% to 18% in 2016, according to the census survey. The Office of National Statistics predicts that, by 2036, over half of local authorities will have a local population aged over 65 in excess of 25% – and there will be a national average of 25% of the population aged over 65 years old by 2046.

Despite the number of older people in the UK, fewer than 0.7% over 65 year olds live in retirement villages, signficantly fewer than in Australia (5.4%) or the United States (6.1%).

The custom built homes in retirement communities are designed with the needs of the older homeowner in mind. The homes are accessible and some even have medical care available on site. Residents are able to live among other older people while maintaining their independence. They have access to shared communal areas and social activities, and some developers even offer the services of a ‘downsizing expert’ or part exchange on your current property.

Those attracted to retirement living may be downsizing after children have left home, suffering with loneliness after the death of a partner, or may just be looking for a less physically challenging living environment in their older years.

However, retirement living and the means of accessing it can be confusing and seem expensive. Indeed, a number of developers keep down the initial up front costs by charging a ground rent or an ‘event fee’, a deferred fee that kicks in after moving out the property and most usually after death.

The Elderly Accommodation Counsel (EAC), in an analysis of Land Registry data for the BBC, found that a significant number of newly built retirement properties lost value on resale.

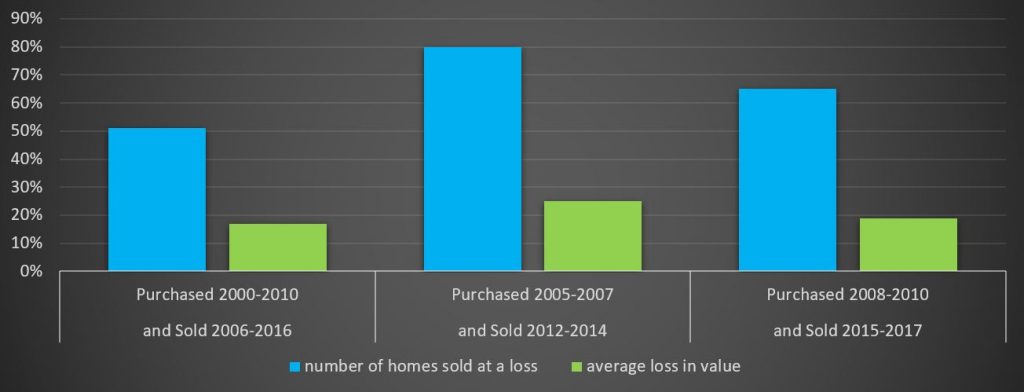

The EAC found that half of newly built retirement homes bought between 2000 and 2010, and sold between 2006 and 2016, fell in value by an average of 17% below purchase price. Of the properties purchased between 2005 and 2007 and sold between 2012 and 2014, four fifths were sold at an average loss of 25% of the purchase price. The situation hasn’t improved much in more recent years, with nearly two thirds of homes purchased between 2008 and 2010 sold at an average loss of nearly 20%.

There are a number of reasons that newly built retirement property might sell at a loss and, though the length of leases must surely be at the top of the list, there are sometimes other reasons. When someone dies, the family often wants to resolve matters quickly and will favour a quick sale over getting the highest price. An ‘event fee’ in the contract may mean that a percentage of the resale value is left to the developer when a person dies or moves out of the property for another reason.

The Law Commission published a report in 2017 which found ‘major problems’ with the use of event fees, although it was accepted that they could assist affordability in the sector. The Commission was also concerned over the use of event fees in circumstances other than selling the home, such as when a carer or spouse moves into the property.

Age UK criticised the lack of transparency over event fees and ground rents, in particular, which were not linked to any obvious benefit for the home owner and were inconsistent between developers.

- Mccarthy and Stone charge an average annual ground rent of £466 for the first 15 years, followed by an increase of 2% or inflation – whichever is higher – and compound annual increase. The ground rents were also sold on to investors by the developer.

- Audley Group charges an average annual ground rent of £500 plus an event fee of 15% of the resale price.

- Churchill Retirement Living charges an average annual ground rent of £500 with a seven yearly inflation increase, plus an event fee of 1% on resale price.

BetterRetirementHousing.com is campaigning on the issue and addressed an All Party Parliamentary Group on leasehold and commonhold reform in July, in which all of the developers defended their practices.

Make sure you ask an independent Chartered Surveyor to inspect the property when you purchase any type of new home.

Back to October 2018 NewsletterÂ

© www.PropertySurveying.co.uk

SH/LCB